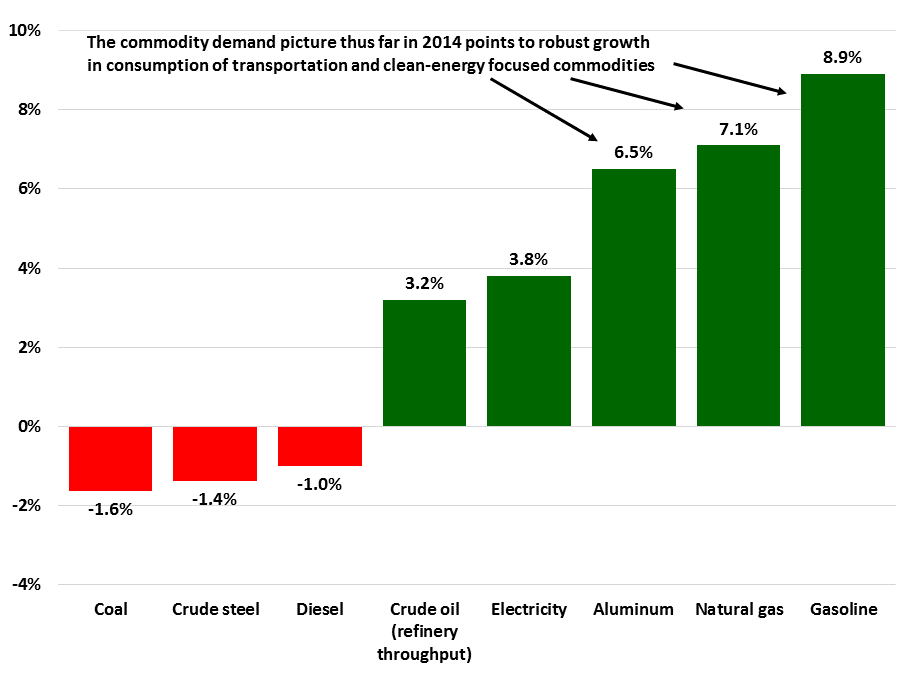

Gasoline, natural gas, and aluminum are China’s commodity demand bright spots so far in 2014—amidst a significant downturn in consumption of key basic materials, namely coal, steel, and diesel fuel. Gasoline consumption in China rose by 8.9% YoY between January and October. These results are not surprising given that new car sales rose nearly 16% YoY during the same time period. Healthy growth in transportation equipment output—especially automobiles, subways, and aerospace items—also drives aluminum demand, and apparent aluminum consumption is up 6.5% YoY in the first 10 months of 2014 (Exhibit 1). Finally, natural gas demand is also growing strongly as large Chinese cities work to clean up their air.

Exhibit 1: China Key Commodity Demand Growth for First 10 Months of 2014, YoY Change

Source: NBS China, local media, China SignPost™

China’s fixed asset investment and heavy industrial activity are clearly slowing. Electricity consumption data—one of the more reliable indicators of economic activity levels—shows that between January and October 2014, China’s “secondary” industries saw their power usage rise by 3.9% YoY. The secondary industries (“第二产业”) encompass most forms of manufacturing, fuel and water production, and construction and account for nearly ¾ of China’s electrical power consumption. In contrast, secondary industries’ power use rose by 6.7% YoY during the first 10 months of 2013, suggesting that activity is expanding much less robustly in 2014.

Taken in conjunction with the fact that demand for diesel fuel (which is used to move goods around the country and to the ports) is also down, weaker electricity demand bears close attention because the electricity demand growth figure is a useful proxy for assessing what “real” economic growth in China is at present.

Likewise, China’s coal and steel demand have turned negative for the first time in decades, signaling that demand is plateauing faster than many—especially the mining companies—expected. Depending on how the first six months of 2015 turn out, it may be appropriate to call “Peak Steel” for China—and possibly, “Peak Coal” as well.

Bottom Line: Global commodity markets are in a new phase, and as China continues to slow, the lowest-cost commodity producers will attract the lion’s share of any capital that remains willing to invest in the commodity space. China’s demand for a number of bulk commodities—particularly metals and coal—is flattening decisively—and events in 2015 will clarify if the trend is temporary or permanent. Our belief is that the plateauing demand for steel, coal, and cement, in particular, is more permanent. The dynamics playing out now align with the S-Curves research we first published in the summer of 2011.