China’s weather so far in Fall 2014 has been relatively mild, in contrast to 2009 and 2013, when November cold waves prompted major gas shortages in much of Eastern and Central China.

The first cold snap this coming winter will very likely set the stage for another round of serious natural gas shortages in many parts of China. CNPC researchers estimate this winter’s gap between supply and demand could grow to 13.6 billion cubic meters—roughly twice as large as last winter’s gap and approximately 42% more gas than was delivered to the municipality of Beijing in the entire year of 2013.

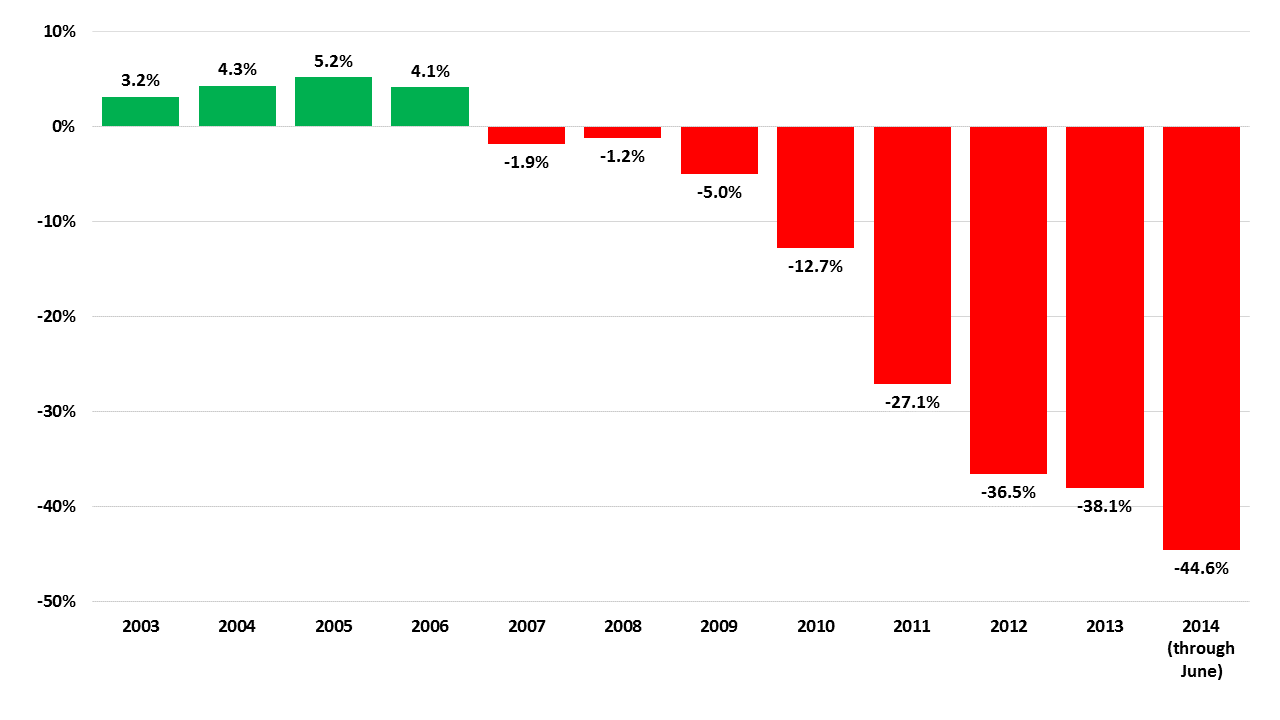

Over the past seven years, China’s gas supply deficit has burgeoned dramatically, and as of June 2014, stood at nearly 45% (Exhibit 1). In recent months, domestic gas supply increases have tapered off and the supply deficit is now likely even more acute than it was during the summer, increasing China’s dependency on pipeline and LNG imports.

Exhibit 1: China Gas Supply Deficit

Shortfall as percentage of domestic production

Source: BP, NBS China, China SignPost™ analysis

This growing reliance poses challenges because import infrastructure is not optimized to respond to rapid demand spikes in China’s populous and increasingly gas-hungry central regions—especially Chongqing, Sichuan, Hubei, Hunan, and Anhui—where many gas demand centers cannot easily access “surge” gas supplies from seaborne LNG imports, the most responsive supply source when sudden demand spikes occur.

CNPC, Sinopec, and others are working to build out gas storage capacity, but China’s storage caverns and tanks still fall short of the coverage ratio the country will need to ensure gas supply security during cold winters—12-15% of total annual demand, as opposed to the roughly 2-3% working coverage now likely in place. To put recent storage capacity additions in perspective, consider that CNPC’s Hutubi storage facility in Xinjiang, which came online in 3Q2013; and Xiangguosi facility near Chongqing, which came online in 3Q2014; can store a combined total of approximately 15 billion cubic meters of gas.

But this capacity is constrained by infrastructure availability and—given the current state of gas trunk pipeline coverage in China—is not well-positioned to augment supplies in much of Central and North-Central China when the full winter chill hits. Hutubi can inject 11.23 million cubic meters per day of extra gas into the pipeline system in Xinjiang and Xiangguosi can put another 10 million cubic meters per day of supplementary gas into the pipelines near Chongqing.

However, in a serious cold snap that ranges across Central and Eastern China, this will likely prove insufficient to restore supply stability. For instance, in January 2013, the city of Wuhan by itself faced peak gas supply shortfalls of 700,000 cubic meters per day, which if multiplied across China’s populous (and increasingly gas-hungry) inland provinces, quickly absorbs the additional gas injections and leaves many areas still short on gas supplies. And if the winter is colder than expected (think U.S. “Polar Vortex” in 2013-14), the city of Chongqing itself, which ran a 20% gas supply deficit this past winter, would likely effectively absorb all of the molecules Xiangguosi injected before they ever made it to consumers further downstream.

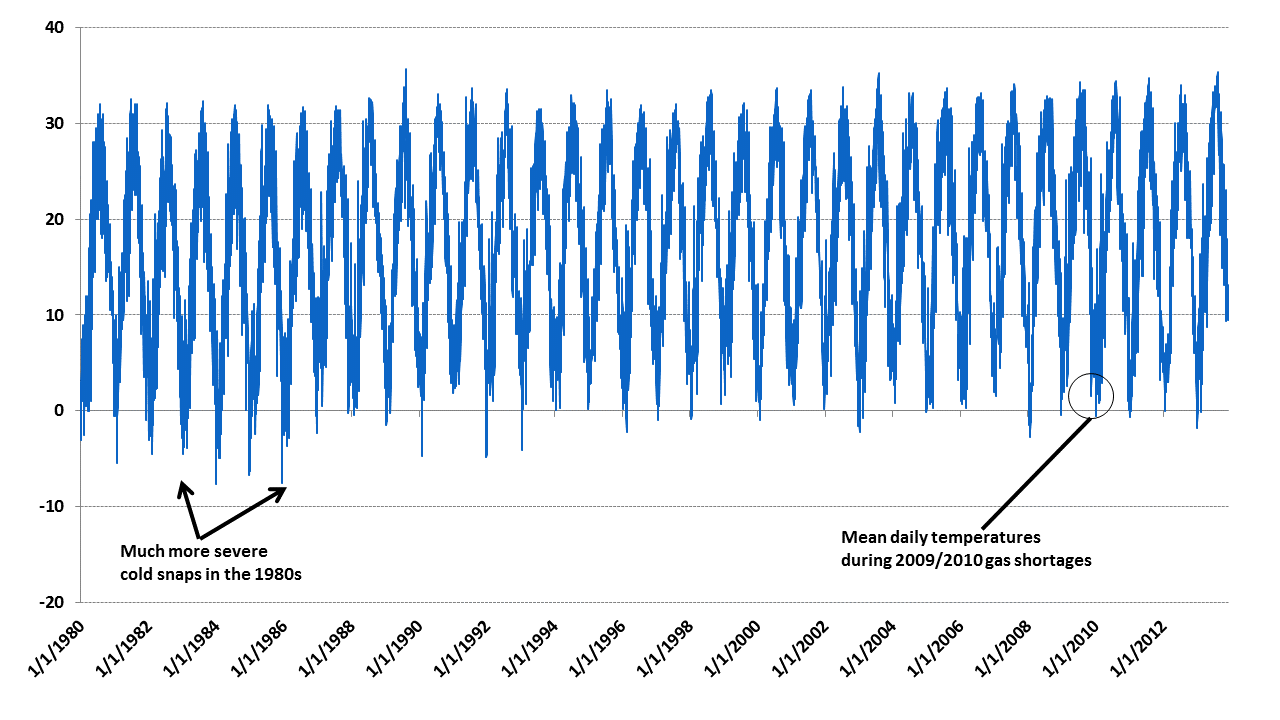

China can get much colder than we have seen in recent winters…

Mother Nature could set the stage for a natural gas supply crunch substantially more serious than the ones China has encountered during the past several winters. Since Central China is an area that has been repeatedly affected by natural gas supply shortages since 2009, when large-scale shortages were first reported, it is worthwhile to assess temperature curves for the region and see how they looked when gas shortages occurred. Perhaps more importantly for assessing risk, examining such historical data—in this case, 33 years’ worth—sheds light on how much worse things could potentially be relative to where they stand now (Exhibit 2).

Exhibit 2: Mean Daily Temperatures for Changsha, Hunan (January 1980-7 December 2013)

Degrees Celsius

Source: AccuWeather, China SignPost™

We chose data for the city of Changsha because it is a sizeable natural gas market and because it lies far enough south that when a cold Siberian air mass makes it into Hunan, we know that it has almost certainly also chilled a vast swath of North and Central China—home to more than 500 million people. As such, a Siberian blast powerful enough to affect Changsha has a very high probability of straining the natural gas supply infrastructure and causing disruptions.

The mean daily temperatures during the very serious 2009 natural gas shortages were in the neighborhood of 0° Celsius. To be sure, this is frigid for a city located at approximately the same latitude as Orlando, Florida and renowned for summers that are as hot as its signature Hunanese cuisine. Yet in the 1980s, several more severe cold snaps hit Changsha, sending the mercury plummeting to the -8° Celsius range.

The demand effects of a cold snap that fell below the range many homeowners are accustomed to would likely boost heating and natural gas demand dramatically, thus exacerbating supply shortages and infrastructure problems that might arise.

A Severe Cold Snap Would Likely Trigger Exponential Increases in Gas Demand

Multiple academic studies show that as temperatures move away from the “room temperature” comfort range (usually around 70°F), demand for energy for climate control such as heating and cooling increases exponentially. A 2°F decrease induces a 4.6% increase in electricity demand. We expect that in parts of China where gas has penetrated into the residential market, such an exponential effect would also apply to gas demand during times of extreme temperature variation.

Bottom Line

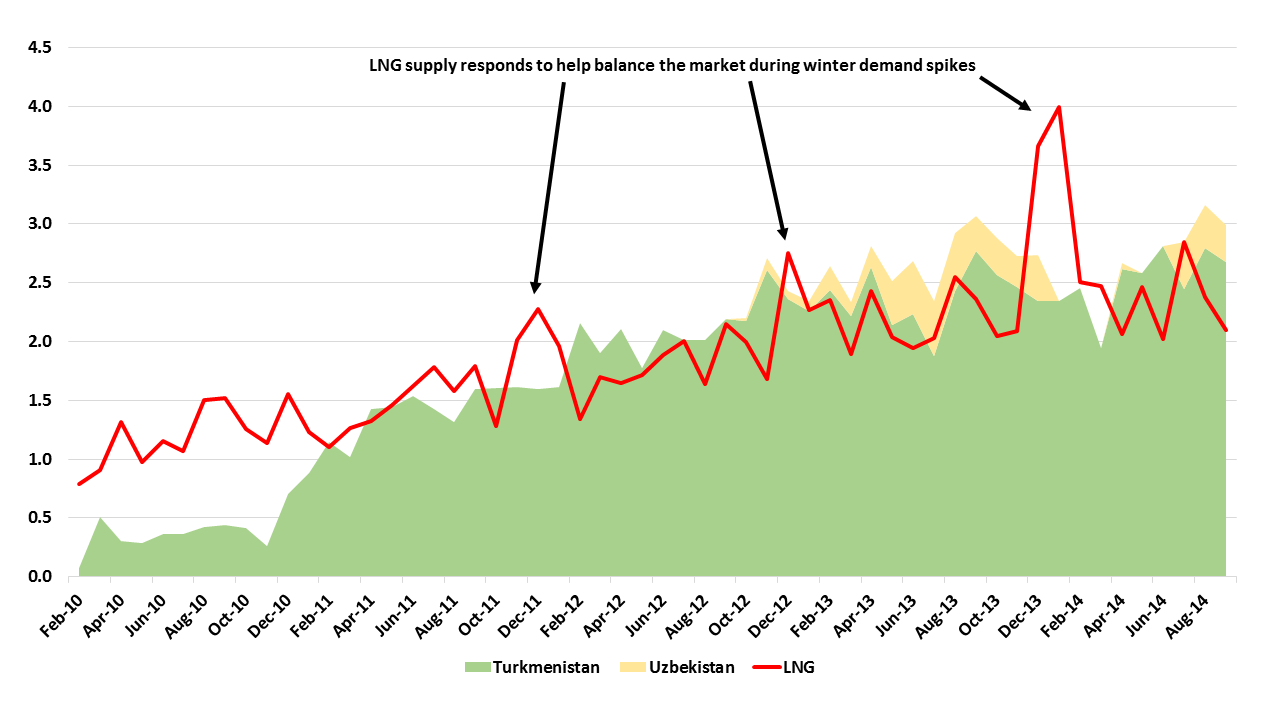

China’s first 2014 cold snap will likely drive a sharp increase in LNG imports, as these quick response supplies can react to market changes much more rapidly and flexibly than pipeline imports can. Last winter, LNG imports into China peaked at nearly 4 billion cubic feet per day (“BCF/d”)—roughly 1.5 times what the municipality of Beijing consumes on peak winter demand days (Exhibit 4). We estimate multiple cold snaps this winter could see LNG imports spike at 4.5 BCF/d in order to rebalance the Chinese gas market, with commensurate positive price impacts in the NE Asian and global LNG markets.

Exhibit 4: LNG and Central Asian Pipelines Both Supply Baseload Gas, but LNG Balances Gas Supplies During Peak Demand Times

BCF/d

Source: NBS China, China SignPost™ analysis