China’s significant natural gas shortage will catalyze greater investment in pipelines, storage, and domestic drilling.

China is suffering a serious natural gas supply shortage as cool weather collides with serious air pollution problems in cities including Beijing, Harbin, and Shanghai.

Local experts

believe the structural gas shortage currently afflicting China will likely endure for at least three more years, even as reforms prioritize using natural gas and eliminating barriers and bottlenecks to its use. We concur with this view based on several key factors.

First, China’s demand for natural gas has exploded over the past several years and continues to rise robustly even as the baseline for comparison gets substantially higher each year. Gas demand is growing especially quickly in the residential sector as companies such as China Gas and ENN rapidly build out their local pipe and supply networks.

As a result of this demand growth, production has not kept pace with rising demand.

NDRC Vice Director Lian Weiliang

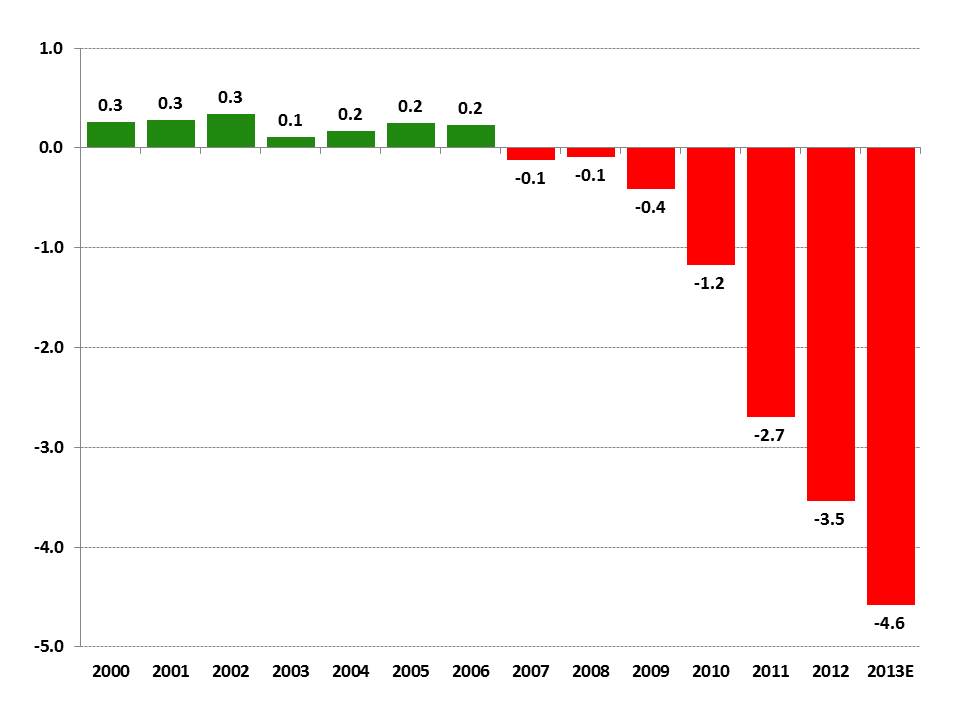

reports that through September 2013, China’s gas consumption expanded 13.5% YoY, while production only grew by 9.2% YoY. We estimate that the deficit between China’s natural gas demand and domestic gas production is now approximately 4.6 billion cubic feet per day (Exhibit 1).

Exhibit 1: China’s domestic gas supply deficit

Billion cubic feet per day

Source: BP, NBS China, China SignPost™ estimate

To put this number in perspective, we estimate this is enough gas to supply the daily gas needs of more than 120 million Chinese households. Alternatively, it would be enough gas to fuel 23 GW of gas fired power generation capacity, which

could displace

251,000 tonnes of steam coal demand per day.

China’s

Third Plenum reforms

are likely to drive further use of liquefied natural gas (LNG) under the rubric of “Beautiful China” environmental conservation and resource pricing initiatives. Previously, LNG consumption was constrained by relatively high prices and limited infrastructure, which produced periodic shortages, particularly in winter months and away from coastal distribution centers.

Now that LNG offers one of the few ways to readily and substantially offset air pollution, China’s government is likely to support its greater use through pricing incentive schemes and constructing coastal LNG terminals and inland pipeline infrastructure (previously major bottlenecks). Yet, as the analysis below suggests, these measures are complex and take time to implement. In the meantime, serious supply constraints will continue to occur.

To be sure, China is not solely reliant on domestically produced gas. It enjoys access to LNG and pipeline gas from Central Asia, and now Myanmar as well. We estimate at present that China currently has approximately 6.0 BCF per day of gas import capacity (2.9 BCF/day by pipeline from Central Asia and 3.1 BCF per day via the country’s LNG terminals). The number is somewhat lower than the LNG terminals’ total nameplate capacity would suggest because several terminals came online in the past two months and we believe they are not yet fully operational.

On this basis, China’s potential natural gas import capacity likely exceeds the present deficit by more than 20%, which raises the question of why there are such problems with gas shortages over the past several winters. We believe the shortages are a product of four core factors—(1) gas demand growth is outpacing pipeline network expansion, (2) China does not have sufficient gas storage capacity to smooth demand spikes triggered by cold weather, (3) Chinese terminals must compete with buyers from Japan and other locations for spot LNG cargoes, and (4) Chinese domestic gas prices need to be liberalized so importers do not lose money on supplies they bring in.

With respect to pipeline constraints, it is very likely that many Chinese LNG terminals are not optimally integrated with gas pipeline infrastructure beyond their immediate surrounding area where their “anchor customers” (typically power plants) are located. This makes it difficult to divert gas supplies in response to demand swings in other regions further away and contributes to the severity of shortages that emerge. Here it bears noting that some of the most heavily utilized LNG terminal infrastructure in Europe is in

France and Belgium

, where LNG regas facilities are very well integrated with pipeline infrastructure that allows imported gas to penetrate deep into the marketplace.

Unlike LNG, China pipeline gas exports from Central Asia flow into a well-connected pipeline network that can move molecules relatively seamlessly from Turkmenistan all the way to Shanghai and Guangzhou. The second

West-East Gas Pipeline

has a trunkline that carries gas from Central Asia and Xinjiang, as well as eight branch lines in Central and Southern China that spans 14 provinces in total. Unfortunately, pipelines are not as able to respond to sudden demand changes as well as LNG terminals can.

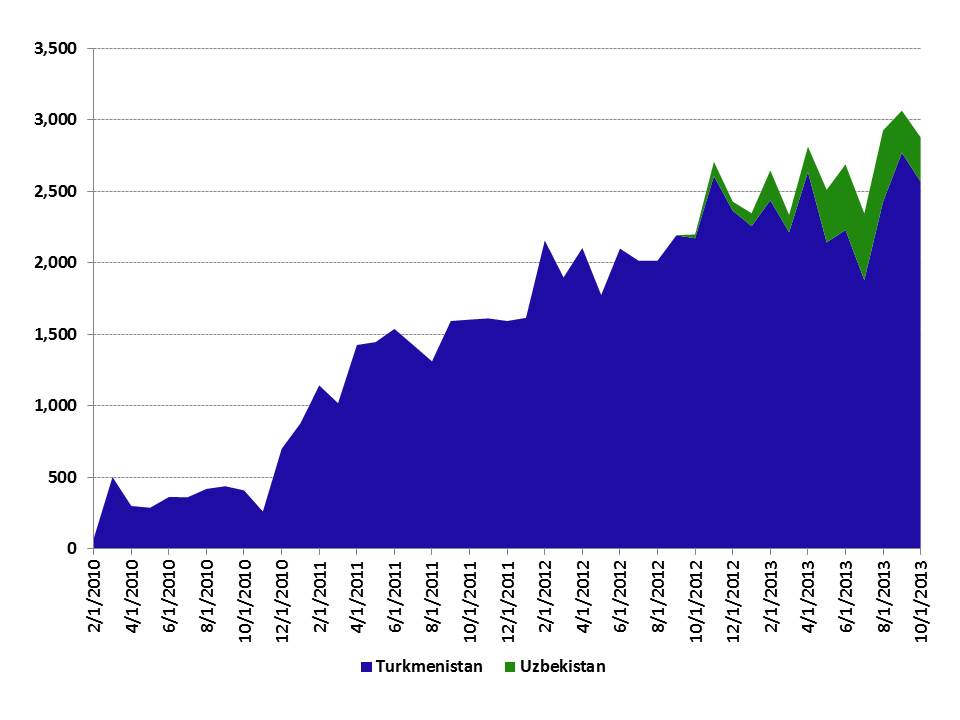

China’s pipeline imports from Central Asia have grown substantially since their commencement in 2010, moving from 74 million cubic feet per day in early 2010 to nearly 2.9 billion cubic feet per day by the end of October 2013 (Exhibit 2). China’s pipeline gas import volumes will grow by an additional 1.1 BCF/day in 2014 as the now completed

Myanmar-to-China pipeline

comes online and further in 2015 and 2016, as additional pipelines carrying gas from

Kazakhstan

come online.

Exhibit 2: Pipeline Natural gas Imports from Central Asia into China

Million cubic feet per day

Source: China Customs

Chinese sources note that Chinese gas inventories are low in relation to the demand pressures that winter cold snaps will put on them. China’s working gas storage capacity is presently only two percent of annual consumption, according to Caixin. In contrast, the highly developed

U.S. gas market

has working storage equal to approximately nine percent of annual consumption. Low working storage helps smooth over wide seasonal demand swings. In Beijing, for instance, local sources say daily gas consumption during the winter is eight times higher than in the summer.

Chinese sources report that Beijing and Tianjin receive approximately half of their peak winter gas supply from a cluster of six underground storage facilities in the Dagang oilfield that have a total capacity of 247 BCF. Based on this data, the Beijing/Tianjin metroplex thus has approximately 7 BCF of storage capacity per million residents. Each Chinese city will have unique local climatic and other conditions, but this gives a starting point for assessing the need for additional inventory buildout.

China’s gas storage buildout will incorporate a mix of system, including underground caverns, depleted oil and gas fields, and small-scale LNG facilities that liquefy gas and then store it for time of shortage. For example, the city of Changsha, which has been afflicted by a number of significant gas shortages since 2009, now has an LNG storage facility that can store 424 million cubic feet of gas.

Xindi Energy Engineering

(新地能源工程技术有限公司), which helped construct the facility in 2011, says it can supply 8-10 days’ worth of gas supply for Changsha.

International Competition for Gas Supplies

Chinese companies wishing to obtain spot LNG cargoes must contend with buyers from Japan and South Korea, who in some ways need the gas even more because they do not have meaningful domestic production. Japan’s decision earlier this year to close all of its nuclear reactors has helped tighten the LNG market and exacerbate competition for spot cargoes.

To help incentivize companies to source gas internationally, the Chinese government recently raised the sale price of imported gas by 26%. The government likely hopes the measure will encourage companies like

CNPC/PetroChina

—which lost roughly US $7 billion on gas sales in 2012—to maximize imports and help alleviate shortages at home. The problem is that the government’s new price is still only about US $5.67/mmbtu, less than a third of the going price for LNG in the Northeast Asian LNG spot market. Similarly, China’s pipeline gas imports from Turkmenistan are priced on an

oil-linked formula

that most likely has them above US $5.50/mmbtu at current crude prices.

It therefore remains to be seen (1) what other incentives the government may have to implement in order to incentivize LNG importers to maximize their terminals throughput and (2) if pipeline infrastructure can get additional supplies from LNG imports to inland markets. We estimate that China’s operational LNG terminal could, at least in theory, bring in an additional 200-400 million cubic feet per day of gas supplies if they can successfully compete for spot cargoes.

Responses so far to the emerging Winter 2013-14 gas shortages

Companies are already responding to the gas shortages. On the demand side, suppliers are curtailing gas deliveries to industrial gas consumers to ensure that the growing number of residential gas consumers will have access to adequate to stay warm this winter.

Indeed, in early November 2013, Sinopec began cutting gas supplies to industrial facilities such as a petrochemical plant and the Qilu refinery in Shandong in order to ensure that it has sufficient gas to meet residential consumers’ needs. We estimate this will free up 1.3 million cubic meters per day of supply—enough gas to supply 14,000-16,000 households through the winter.

Based on the relatively cosmetic macro-level impact of such industrial curtailments, we believe there will likely be a much larger number of industrial and power generation gas users who are forced offline this winter in order to prioritize residential gas supplies. We believe the most acute shortages will be in SW China, NE China, and parts of Central China not near the West-East trunk gas pipelines. These are the areas with the least access to gas supplies such as LNG that can be “surged” in response to cold weather and other demand stimuli.

Domestic production “balancing” is likely to end in 2014

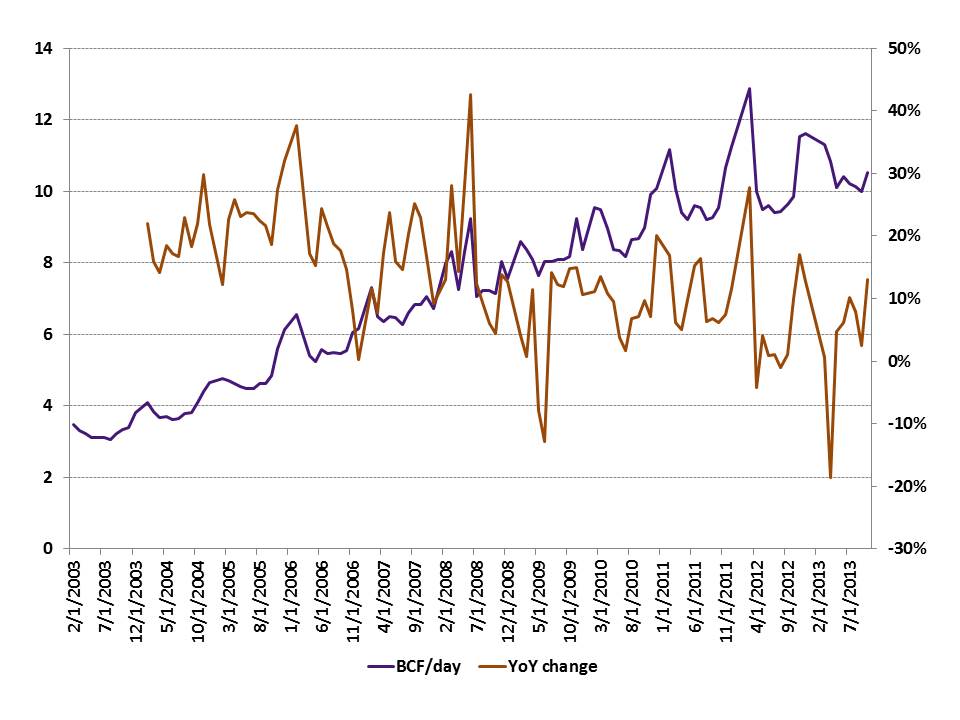

China’s Big Three oil & gas companies have also been instructed to maximize natural gas output. Earlier in the year, and in 2012 as well, PetroChina in particular, appeared to be altering its domestic production up and down in response to demand because much of its LNG and pipeline gas import volumes were coming on a “take or pay” fixed volume basis. Therefore, it was more economical for the company to swing its domestic fields and use them as a balancer. Now, however, the Chinese gas market is tightening enough that the big spring drop-offs in domestic gas production seen in 2011 and 2012 will likely come to a permanent end. Indeed, 2013 showed a much smaller spring drop-off than 2012 did and we expect that in 2014 this drop will be much smaller than it was in 2013 (Exhibit 3).

Exhibit 3: China Domestic Natural Gas Production

BCF/day (left axis), YoY change (right axis)

Source: NBS China, China SignPost™

What does the rest of this winter portend for China’s gas market?

Our view is that the shortages currently affecting the Chinese natural gas market will worsen as the winter deepens. Industrial users will bear the brunt of supply cuts as the government sacrifices them by decree in order to protect China’s growing ranks of residential gas consumers.

LNG is the most “surge-able” form of natural gas supply in China.

CNOOC

is bringing a new 2.2 mtpa floating LNG terminal online off Tianjin, which is slated to take its first cargo in December 2013 and could help alleviate local gas supply shortfalls later in the winter as it ramps up. With the pipeline from Central Asia unable to surge production and domestic fields running hard, we expect LNG exports to rise as China fights to keep the gas market supplied.

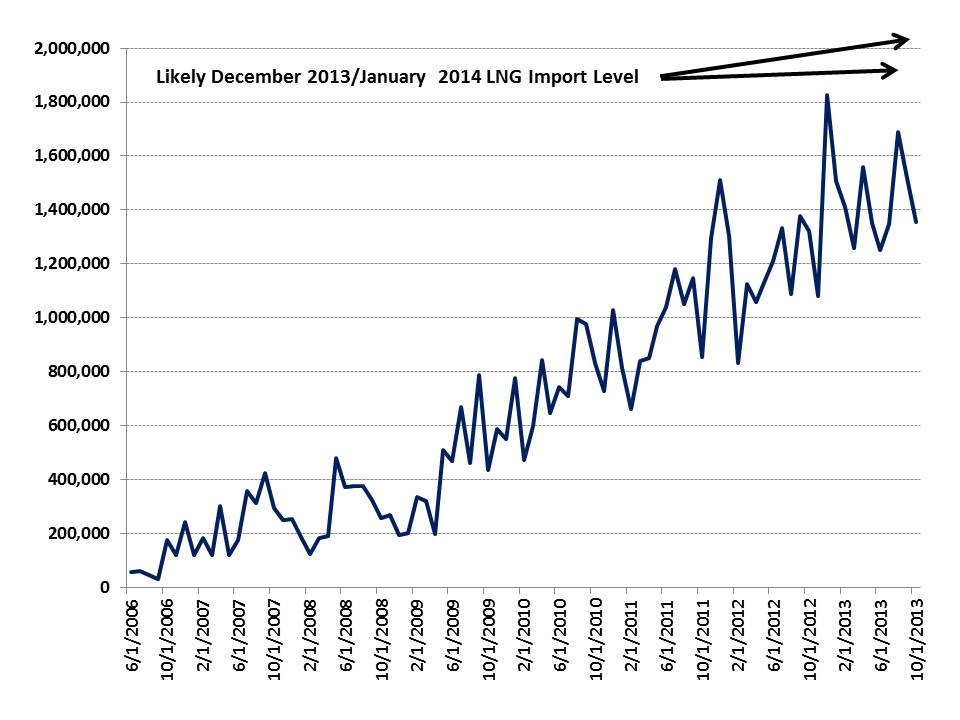

In 2011 and 2012, December was the largest volume month of the year for LNG imports. As Exhibit 4 (below) shows, 2013 looks poised for a bigger year than the prior two. We therefore believe there is a high probability that December 2013 LNG imports into China could break the 2 million tonnes mark. The prior historical high is 1.8 million tonnes. The fact that industrial facilities were already being kicked offline by fiat by mid-November reinforces our conviction, as there are four solid cold months to go in northern China.

Exhibit 4: China LNG Imports

Metric tonnes per month

Source: Gen. Admin. Customs

China can get much colder than it is now…

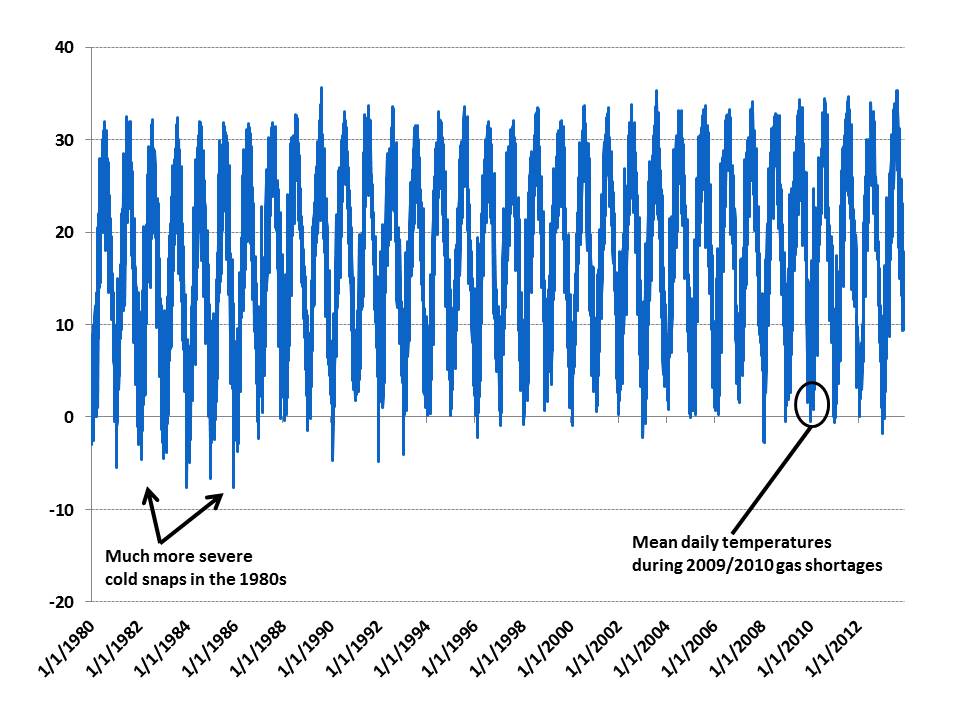

In conclusion, we call your attention to historical weather data, which suggests Mother Nature could set the stage for a natural gas supply crunch substantially more serious than the one China is grappling with now. Given that Central China is an area that has been repeatedly affected by natural gas supply shortages since 2009, when large-scale shortages were first reported, it is worthwhile to assess temperature curves for the region and see how they looked when gas shortages occurred. Perhaps more importantly for assessing risk, examining such historical data—in this case, 33 years’ worth—sheds light on how much worse things could potentially be relative to where they stand now.

We chose data for the city of Changsha because it is a sizeable natural gas market and because it lies far enough south that when a cold Siberian airmass makes it into Hunan, we know that it has almost certainly also affected a vast swath of North and Central China—home to more than 500 million people. As such, a Siberian blast powerful enough to affect Changsha has a very high probability of straining the natural gas supply structure and causing disruptions.

The mean daily temperatures during the very serious 2009 natural gas shortages were in the neighborhood of 0° Celsius. To be sure, this is frigid for a city located at approximately the same latitude as Orlando, Florida and renowned for summers that are as hot as its signature Hunan cuisine. Yet in the 1980s, several more severe cold snaps hit Changsha, sending the mercury down to the -8° Celsius range.

The demand effects of a cold snap that went beyond the range many homeowners are accustomed to would likely boost heating and natural gas demand dramatically.

Multiple academic studies

show that as temperatures move away from the “room temperature” comfort range (usually around 70F), demand for energy for climate control such as heating and cooling increases exponentially—i.e. a 2° F change induced a 4.6% increase in electricity demand. We expect that in parts of China where gas has penetrated into the residential market, such an exponential effect would also apply to gas demand during times of extreme temperature variation.

Exhibit 5: Mean Daily Temperatures for Changsha, Hunan (January 1980-7 December 2013)

Degrees Celsius

Source: AccuWeather, China SignPost™

Additional Research:

–Gabe Collins and Andrew Erickson, “

Central and Southwest China: The Key Battleground for Shale Gas and New Low-Cost Coal Supplies from Xinjiang, Mongolia, and Wyoming

”,” China SignPost™ (洞察中国), No. 67 (28 September 2012).

–Gabe Collins and Andrew Erickson, “

China Aims to More Than Triple Its Oil & Gas Production in the South China Sea over the Next 10 years

,” China SignPost™ (洞察中国), No. 31 (3 April 2011).

–Gabe Collins and Andrew Erickson, “

China’s Natural Gas Approach: pipelines are best way to resolve shortages

,” China SignPost™ (洞察中国), No. 10 (10 December 2010).