Gabriel Collins,” What If China Ceases To Be The Global ‘Oil Consumer of Last Resort?‘ China SignPost™ (洞察中国) 100 (13 November 2019)

What happens to the world oil market if China can no longer serve as the “consumer of last resort?” The question is uncomfortable to contemplate, but is increasingly relevant as a longer-term structural slowdown in Chinese growth becomes more likely.

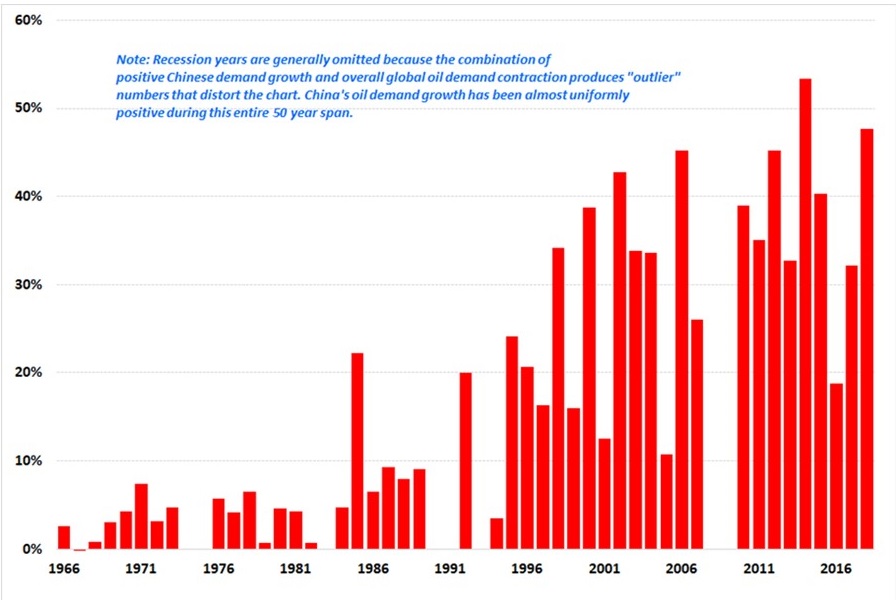

In the past 15 years, China accounted for about 40% of net global oil demand growth.[1] The country’s consumption increase between 2003 and 2018 amounted to about 7 million barrels per day–roughly equivalent to the volume of oil that Brazil, Russia, and Malaysia together consumed per day in 2018.[2] What’s more, oil demand in China continued to grow even during recessions such as 2008-2009 when overall global demand declined, suggesting the actual market impact of Chinese consumption is even larger than the net demand numbers indicate.

Since the late 1990s, oil producers worldwide have increasingly depended upon Chinese demand to absorb the barrels they produce and send into the global marketplace (Exhibit 1). China’s economic expansion over the past 4 decades has been remarkable. But it is increasingly likely over the next decade that the country’s exceptional run will taper off and that growth rates will revert to something closer to the global mean GDP growth rate.[3] As tracked by the World Bank, this figure averaged just under 3% annually from 2003 to 2018.[4] If China slid onto a 3-to-4% annual economic growth trajectory (perhaps ranging lower) and its oil demand downshifted commensurately, the global oil market impacts would be momentous.

Exhibit 1: China as a % of Annual Net Global Oil Demand Growth, 1966-2018

There is a “chicken and egg” aspect to the prior statement, as China’s explosive oil demand uptick in 2004 helped set global oil prices on the path to the nearly $150/bbl level achieved in the summer of 2008, which in turn helped catalyze the US shale oil boom. But the common thread is that whether Chinese demand for crude oil is the “chicken” or the “egg” that hatched it or a little bit of each, removing one or the other breaks the lifecycle. And here that lifecycle implicates a global market that now trades nearly 100 million barrels per day of crude oil worth nearly $2 trillion annually at today’s prices, and whose price movements influence industrial value chains worth trillions of additional dollars and dozens of other critical global commodities and fundamental economic benchmarks.

How Did China’s Oil Demand Get To Where It Stands Now?

Several factors have driven China’s explosive economic growth over the past 25 years. First, the country started from a low baseline.[5] Second, there was a ready supply of underemployed rural workers who moved to cities in search of employment opportunities. Moving rural workers into an industrializing urban setting can raise their productivity by a factor of 3-to-6 times.[6] Third, foreign technology–whether transferred voluntarily, under duress, stolen, or purchased–has been easily accessible. Technology access facilitated high-velocity “catch up” growth as existing, proven technologies were combined with the cheap labor then available in China and in some cases, incrementally innovated upon. Fourth, an artificially low cost of capital in China helped facilitate government policy that obsessively promoted large investments in fixed-assets such as roads, bridges, and buildings, even if the demand to fill them might not come for years after construction.[7]

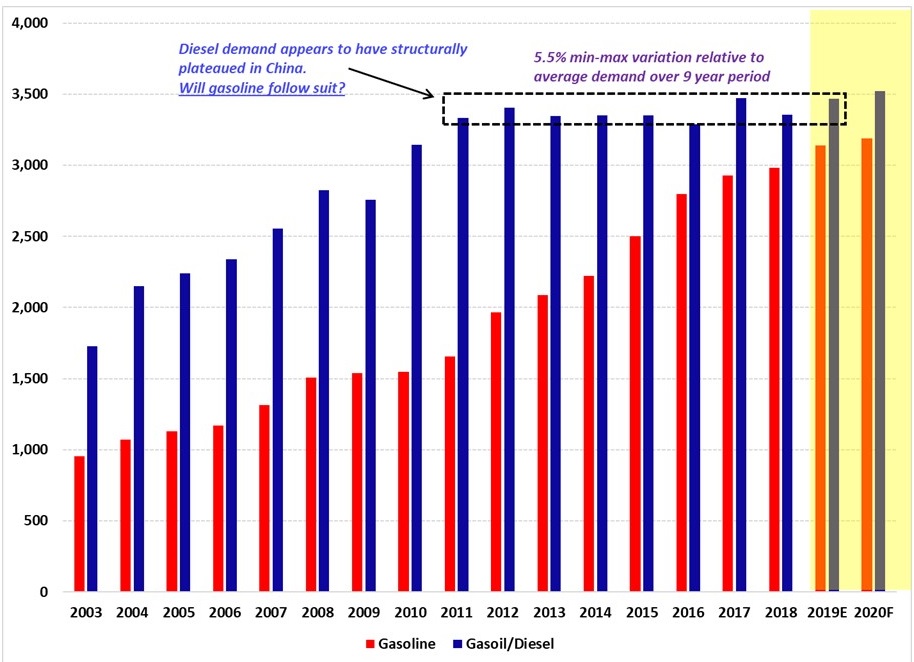

From an oil demand perspective, the confluence of the aforementioned factors yielded two distinct oil demand epochs, which overlapped in the mid-2000s. Diesel fuel, closely linked to industrial and construction activity, dominated Epoch 1. But diesel fuel demand has likely structurally peaked in China on the back of slowing industrial growth.[8] Rising personal car sales beginning in 2005-2008 ushered in Epoch 2 of China’s oil demand expansion–the gasoline era. Epoch 2 continues, but gasoline demand growth is slowing more sharply than many experts have forecast over the past several years.[9] Consider that China’s passenger car fleet rose by 130% and gasoline demand by 50% between 2012 and 2018, but that with a 27% increase in the car fleet between 2016 and 2018, gasoline demand only rose by 6%.[10]

Exhibit 2: China Diesel and Gasoline Demand Profiles, 2003-2020 (Forecast), ‘000 Bpd

Source: IEA OMR

Several potential macro-level factors may explain the gasoline demand growth rate slowdown, including (1) slowing or declining vehicle utilization as drivers confront worsening traffic congestion across many cities in China; (2) greater use of EV’s including small, low-speed units; (3) greater use of non oil-derived “gasoline extenders” such as ethanol and methanol; and (4) greater use of ride sharing services that potentially consolidate gasoline demand into a pool of more efficient vehicles.[11]

It is also possible–although thus far unproven by data–that the slowdowns in car sales and gasoline demand growth in China may also reflect the early phase of an ongoing demographic turnover in which China is aging fast and “turning gray before getting rich.” The effects of such a dynamic could be magnified if as some analysts suspect, Chinese government statisticians have substantially over-counted the country’s population.[12] Even if the Chinese population statistics are reasonably accurate–and the evidence increasingly suggests this is a dubious “if”–the data show a rapidly aging population that could be headed for a Japanese-style demographic crash, albeit without having achieved a per-capita wealth level anywhere close to Japan’s.

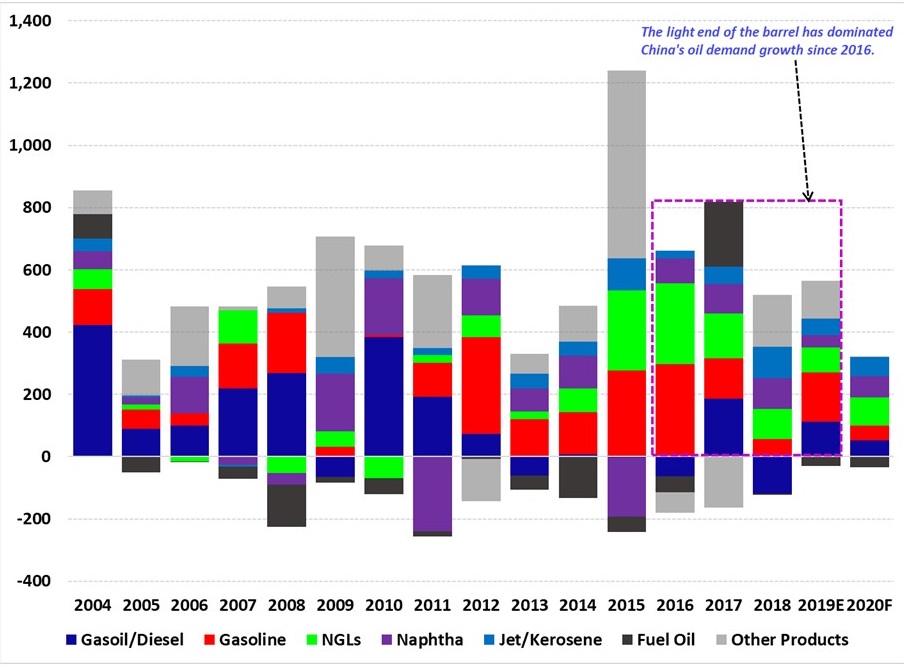

Demographic evolutions are extremely important for consumption growth at the “light end” of the barrel–gasoline, NGLs, and light ends that are building blocks for petrochemicals and gasoline blending components. Pertinently for China, light ends became important contributors to the country’s incremental oil products demand growth in the 2012 timeframe as diesel demand growth slowed down. And by 2015-2016, the light ends became the dominant oil products demand driver (Exhibit 3).

Exhibit 3: China Incremental Oil Demand Growth, By Product

Source: IEA OMR, Author’s Analysis

On the demographic front, trends in China raise concerns about demand for gasoline and other consumer-driven light ends over the next 10-to-15 years. Current on the ground conditions in major Chinese car markets are already prompting prospective car purchasers to reconsider, or causing existing car owners to drive less. Concurrently, China’s wealthier East Coast provinces already consume plastics at a rate on par with much of the OECD world.[13] Poorer provinces in China’s interior and west appear to hold the potential for driving significant upside demand for plastics and other petrochemicals. But unfolding demographic trends may smother this latent demand potential.

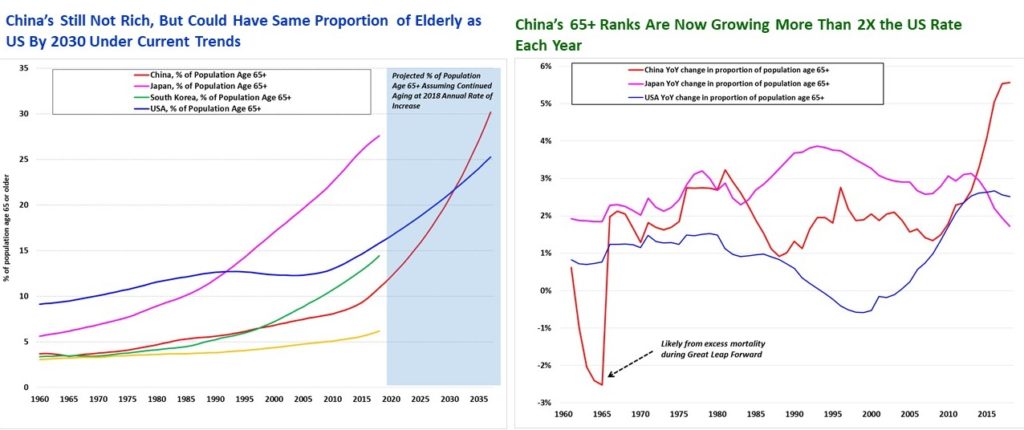

Indeed, China is by at least one core measure now aging twice as rapidly as the US. A straight-line projection of the past two years’ average annual increase in the proportion of China’s population age 65 years or older suggests that China could surpass the US elderly population by 2030 (Exhibit 4). Even if China’s remaining workers become far more productive in coming years by leveraging artificial intelligence and other technological breakthroughs–a very uncertain prospect–they likely will not spend their gains on additional gasoline and plastics.

Exhibit 4: China’s Demographic Trends Extremely Concerning For Prospects of its Consumer Economy and Associated Oil Demand

Source: World Bank, Author’s Analysis

If unfavorable demographics, road congestion, and other factors were to close out the China gasoline era sooner than originally expected, it is unclear that a new demand source (or sources) could emerge soon and with enough scale to launch oil demand Epoch 3. Jet fuel will remain a much smaller market than either diesel or gasoline. Petrochemicals also have limited upside, both because China’s per capita plastics use rate is already on par with US levels and because an increasing amount of petrochemical plant feedstock in China comes not from crude oil, but from natural gas liquids and to a lesser, but still meaningful extent, coal.[14]

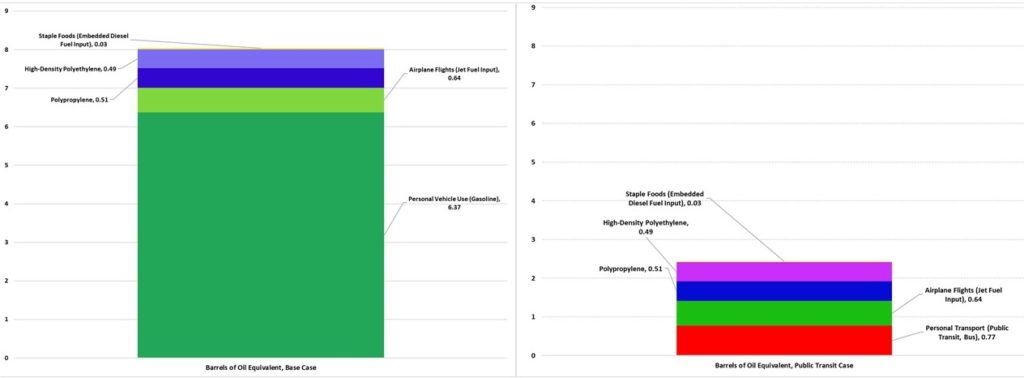

To sharpen the point, we’ve modelled what the annual crude oil demand footprint of a “typical” urban Chinese consumer might plausibly look like. We estimate food-related crude oil footprints on the basis of how much diesel fuel is likely needed to plant, till, and harvest the corn, rice, soybeans, and wheat a typical urbanite would consume in a year, plus how much fuel is likely needed to transport those crops to market. For vegetables, we use a crop budget showing estimated fuel use of a commercial tomato farming operation in California’s San Joaquin Valley near Fresno. For meat, we apply an estimated feed conversion ratio to calculate how many kilograms of grain (and by extension, how much diesel fuel) are embedded in the meat Chinese consumers are eating.

For dairy products, we assume that cows are fed a mix of alfalfa, corn, and soy as detailed in data from the University of Arkansas. We use a crop budget from Texas A&M to calculate how much diesel fuel is likely required to produce a given tonnage of alfalfa. For plastics, we use various data sources indicating the total embedded energy content for high-density polyethylene and polypropylene and multiply this by data from ICIS estimating the total annual plastics demand of consumers in Beijing for the year 2016. To make the plastics data, which are a “derivative” oil use, directly comparable to “consumptive” oil uses, we calculated each oil use’s heat content in BTU and converted that into “barrels of oil equivalent” at the commonly used rate of 6 million BTU per barrel of crude oil.[15]

Exhibit 5: Annual Crude Oil Use Footprint of an Urban Chinese Consumer Who Owns a Car and One Who Doesn’t, Barrels/yr of Oil Equivalent

Car Owner Non-Car Owner

Source: Academic Publications (available upon request), ICIS, NBS China, USA Today, Author’s Estimates

Can Any Other Oil Demand Sources Credibly Compensate for a Significant Loss of Chinese Consumption During the Next 5 Years?

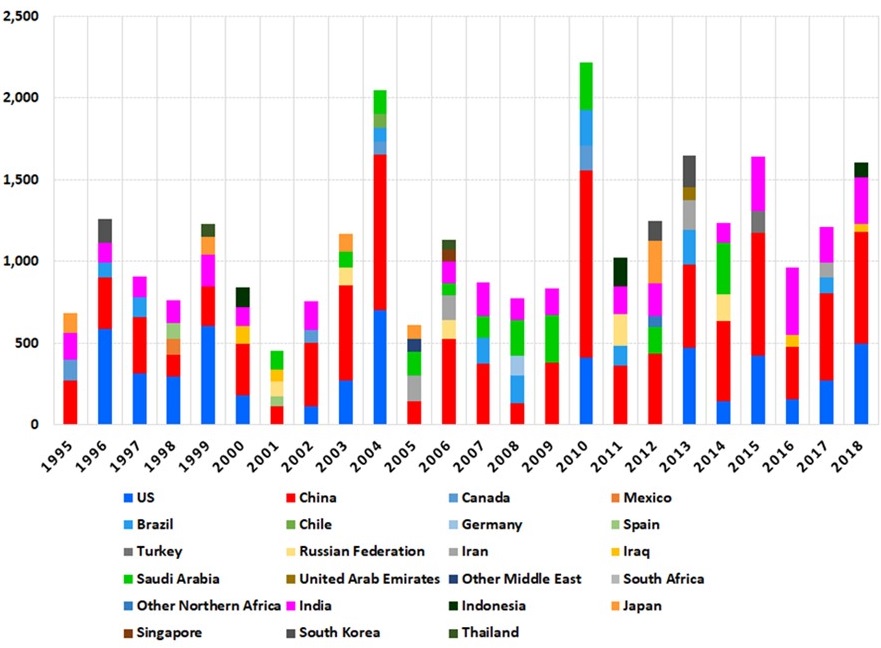

Maybe. Since 1995, China has persistently been one of the world’s largest single sources of oil demand growth (Exhibit 6). In the late 1990s, the US also helped drive global oil demand increases, but since 2006, China has generally been the biggest game in town. Of the regions whose growth is not leveraged as heavily to China (more on this in a moment), India is the primary high-potential demand offsetter. As India invests more in transportation infrastructure passenger car ownership rises, and personal cars become more popular modes for long-distance intercity travel, the country’s oil products demand is likely to continue rising robustly.[16] And unlike the commodity exporter we’re about to discuss, lower oil prices caused by a Chinese growth slowdown would likely actually stimulate greater oil consumption in India.

Exhibit 6: Top 5 Oil Demand Growth Countries by Year Since 1995, ‘000 Bpd

Source: BP Statistical Review of World Energy 2019, Author’s Analysis

The other key takeaway from Exhibit 6 is that in many years, the key secondary drivers of oil demand growth globally have been the commodity producing countries that most benefited from China’s skyrocketing demand during the past 15 years. In this sense, China’s boom had a “multiplier” effect on global oil demand growth. Indeed, this author’s calculations indicate that between 2003 and 2014 (when oil prices crashed), China’s own oil demand grew by about 5.4 million barrels per day. But the combined oil demand growth in Africa, Central and South America, the Former Soviet Union, and the Middle East (commodity exporting regions heavily leveraged to Chinese growth) clocked in at 7.3 million barrels per day–1.3 times China’s own demand growth.

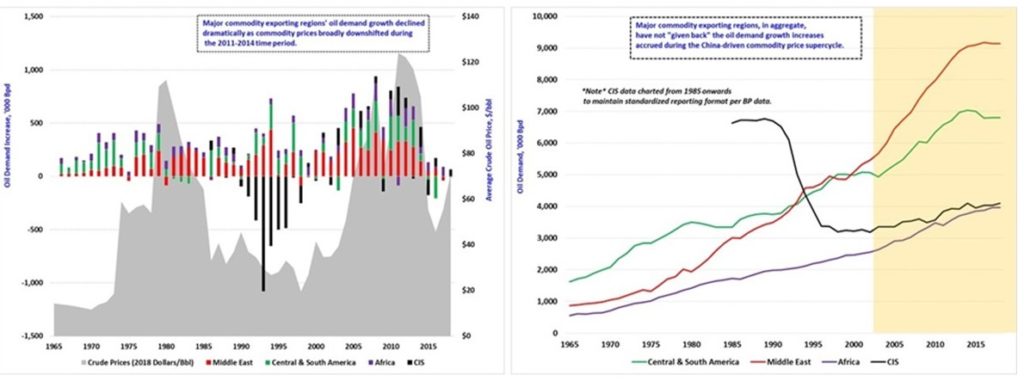

These regions’ oil demand growth has slowed dramatically since the commodity supercycle began to wane in 2011-2012, and plummeted along with crude oil prices in 2014. Thus far the major commodity exporting regions, in aggregate, have not “given back” the oil demand growth increases accrued during the China-driven commodity price supercycle (Exhibit 7). And therein lies a core fear about what could happen if China’s economy truly turned over–it would not just be Chinese oil demand lost, but also consumption from the constellation of major global oil exporters and basic commodity suppliers who have grown their own economies in recent years by feeding China’s hitherto insatiable hunger for raw materials.

Exhibit 7: Oil Demand Growth in China’s Supplier Regions Exceeded China’s Own During the Boom Years–And Has Not Yet Been “Given Back” Despite Low Oil Prices

Source: BP Statistical Review of World Energy, Author’s Analysis

Just as China’s oil and commodity demand growth induced global “multiplier” effects through income increases and economic growth in oil-exporting countries, a significant Chinese oil demand decline would also very likely induce multiplier effects–albeit negative ones. In the oil market, even relatively small percentage departures from trend can have outsized effects on prices. For instance, the global oil supply surplus during the deepest phase of the 2014–16 global oil price crash was only about two million barrels per day (less than 5% of total global demand), and prices still fell below thirty dollars per barrel at their nadir.

A sustained sub-$40 oil price environment due to an unexpectedly fast Chinese oil demand slowdown would likely be profoundly destabilizing in key commodity exporting regions, including the Greater Middle East, Africa, and Latin America. Extreme instability would provide some degree of price support if unrest took oil supplies offline–as was the case with Libya in 2010 and 2011–but restoring demand is a much tougher slog than tweaking supply via OPEC actions. And if Chinese oil demand becomes constrained by basic demographic factors, that cannot be fixed even over the course of many years. India cannot generate sufficient growth to compensate for the loss of Chinese demand, and many developing countries that have been driving crude oil demand growth aside from China would themselves risk being thrown into depression from loss of Chinese commodity demand.

Conclusion

Since the US first imposed China-specific tariffs in July 2018, the two titans’ bilateral trade conflict has been a focal point for oil market watchers.[17] Trade patterns can reset relatively rapidly. But China’s incipient demographic crisis could potentially be worse than Japan’s, may already be creeping into the oil demand numbers, and is coming on at high velocity.

China’s growing debt load, intensifying political repression, and foreign pushback against the country’s techno-mercantilist practices will accelerate demographic trends’ erosion of the country’s economic growth prospects. The probability of a structurally-driven growth slowdown in China increasingly looms as a transformational–and underappreciated–downside risk to global oil demand and prices.

A key follow-on question for this research is “what are the most likely scenarios for the interplay between declining investor interest in the long-cycle oil projects that underpin global supplies and complex demand-side dynamics such as a potential structural China slowdown?” Within the resulting fairway, we will likely find a plausible set of oil price paths for the next 10-15 years. Investors may currently view oil as “the new tobacco,” but many empirical signals point to oil playing a cornerstone role in the global energy supply portfolio for decades to come. Buckle up for a fascinating ride!

*Note* The opinions and conclusions expressed in this analysis represent the authors’ private views only. They in no way reflect the official positions of Rice University’s Baker Institute for Public Policy, the U.S. Naval War College, or Harvard University.

[1] Calculated using data from the BP Statistical Review of World Energy 2019, https://www.bp.com/en/global/corporate/energy-economics/statistical-review-of-world-energy.html

[2] Ibid.

[3] Pritchett, Lant & Summers, Lawrence H., 2013. “Asia-phoria meets regression to the mean,” Proceedings, Federal Reserve Bank of San Francisco, issue Nov, pages 1-35. https://www.nber.org/papers/w20573

[4] “GDP Growth (annual %),” World Bank, https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG

[5] J. Stewart Black and Allen J. Morrison, “Can China Avoid a Growth Crisis?,” Harvard Business Review, September-October 2019, https://hbr.org/2019/09/can-china-avoid-a-growth-crisis

[6] R. Stephen Brent, “How China Rode the Foreign Technology Wave,” The American Interest, 22 October 2019, https://www.the-american-interest.com/2019/10/22/how-china-rode-the-foreign-technology-wave/

[7] See, for instance: Linda Poon, “China’s Huge Number of Vacant Apartments Is Causing a Problem,” CityLab, 27 February 2019, https://www.citylab.com/equity/2019/02/china-vacant-apartments-housing-market-bubble-ghost-cities/583528/

[8] Gabriel Collins, “China Peak Diesel Poses a Serious Challenge to Saudi Arabia, May Help Force OPEC Production Cut,” China SignPost™ (洞察中国) 94 (5 April 2016), http://www.chinasignpost.com/2016/04/05/china-peak-diesel-poses-a-serious-challenge-to-saudi-arabia-may-help-force-opec-production-cut/

[9] See, for instance a report in which Credit Suisse believed that China’s gasoline demand would increase by between 280 kbd and 360 kbd in both 2016 and 2017, as opposed to actual growth of 298 kbd in 2016, but then only 130 kbd in 2017. (“Connections Series: Oil and…Chinese Consumers,” Credit Suisse, 19 November 2015, Global Equity Research.)

[10]Gabriel Collins,“China’s Gasoline Demand Growth: Is Recent Deceleration Near-Term Noise or Early Stages Of a Structural Shift?,”Baker Institute Research Presentation, March 2019, https://www.bakerinstitute.org/research/chinas-gasoline-demand-growth-recent-deceleration-near-term-noise-or-early-stages-structural-shift/

[11] Ibid.

[12] Wendy Wu, “China may have 90 million fewer people than claimed (that’s twice of Spain’s population),” South China Morning Post, 23 May 2017, https://www.scmp.com/news/china/policies-politics/article/2095311/china-population-much-smaller-you-think-researchers-say (citing University of Wisconsin-Madison demographer Yi Fuxian)

[13] John Richardson, “China polyethylene demand forecasting: Forget GDP, look downstream and focus on regions,” ICIS, 12 March 2019, https://www.icis.com/asian-chemical-connections/2019/03/china-polyethylene-demand-forecasting-forget-gdp-look-downstream-and-focus-on-regions/

[14] Gabriel Collins, “A Growing Portion of China’s “Oil Products” Demand Growth Does Not Actually Come From Crude Oil,” Baker Institute Issue Brief, 20 September 2017, https://www.bakerinstitute.org/files/12161/

[15] Potential error factors in the crude oil footprint analysis: The crop oil footprint analyses omit pesticide use under the assumption that the oil inputs are less than the diesel fuel needs. Fertilizers are omitted because most nitrogen fertilizers are produced using either natural gas feedstock, or in some parts of China, coal. This could comprise a significant source of error and make our food production oil usage numbers overly conservative. In addition, the olefin feedstocks for plastics can be manufactured from crude oil, natural gas, or coal. This analysis assumes that naphtha from crude oil is the primary feedstock for HDPE and PP made and consumed in China, as has traditionally been the case in East Asia more generally. However, polymers are traded in a fungible global market and an increasing proportion of global supplies are derived from natural gas and natural gas liquids from the US. China also has a meaningful amount of internal olefin production derived from coal feedstock. As such, a meaningful proportion of plastics consumed in China at any given point in time may in fact not be produced using crude oil.

[16] Malini Goyal, “How car ownership is changing rapidly and irreversibly in India,” The Economic Times, 21 October 2018, https://economictimes.indiatimes.com/industry/auto/auto-news/how-car-ownership-is-changing-rapidly-and-irreversibly-in-india/articleshow/66296079.cms

[17] “The US-China Trade War: A Timeline,” China Briefing, 5 November 2019, https://www.china-briefing.com/news/the-us-china-trade-war-a-timeline/