Executive Summary:

–Three key factors characterize the “new normal” of China’s oil demand: (1) overall annual oil products demand growth will likely slow from an average of nearly 5% annually to one closer to 2.8% between now and 2020; (2) the country’s oil demand profile has become primarily gasoline-driven, and (3) oil refinery overcapacity is making China one of the world’s largest net exporters of refined products, a trend likely to continue looking out to 2020.

–In 2016, China’s incremental crude oil demand will likely increase by approximately 360 kbd—roughly the average daily consumption of the Philippines.

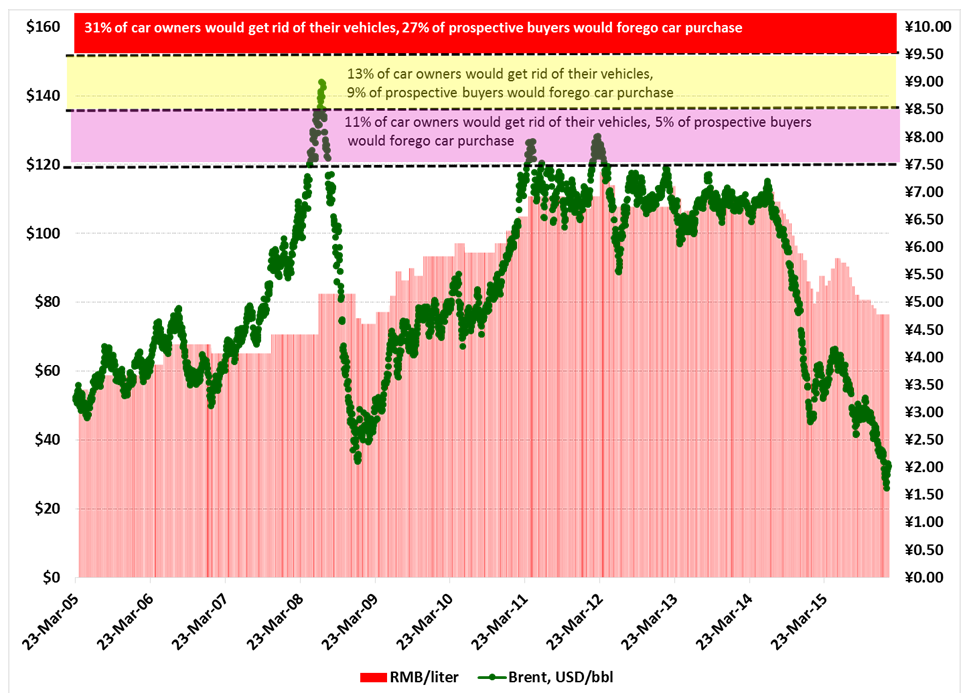

–China’s oil demand is becoming increasingly consumer-driven. Gasoline has become the prime mover of China’s oil demand as car ownership rises and industrially-driven diesel use declines. Rising domestic air travel has also significantly increased kerosene demand, although the macro impact is not nearly as large as that of gasoline.

–Consumer-driven oil demand is likely to be significantly more volatile in the short-term. Consumer sentiments and behavior evolve and shift much more rapidly than China’s traditional oil demand pattern, which was underpinned by industrial diesel fuel use and was closely tied to the 5-Year Plans. Greater demand-side volatility in China stands to have profound effects on the global crude oil and refined products markets—particularly if the Chinese government does not become more regular and transparent in its disclosures of energy data. Better disclosure would reduce market participants’ need to speculate as to the true state of supply and demand balances within the Chinese oil ecosystem. This is turn would help smooth the spikes as prices respond to market fundamentals, benefitting producers and consumers.

–Three core “wild cards” merit close attention over the next five years for their ability to influence China’s oil demand trajectory: (1) road congestion that may reduce vehicle use despite continuing strong sales of new cars, (2) penetration of more efficient gasoline-powered vehicles and electric vehicles as China’s growing middle class pushes back against severe air pollution in many cities, and (3) the degree to which an increasingly brittle Chinese political leadership can craft successful, sustainable solutions to multi-dimensional economic policy challenges.

–Policymaking missteps that accelerate declines in China’s economic growth rate would substantially enhance the risk that prices continue to trade in a narrow band. Currently, the most likely scenario is that a slowing—but still relatively oil-thirsty—Chinese economy combines with deep global CAPEX cuts and marginal costs of new supply exceeding $65/bbl to yield a global benchmark crude oil price range averaging $60-70/bbl between now and 2020.

Full study publicly available at:

Gabriel Collins, “China’s Evolving Oil Demand,” Working Paper, Baker Institute for Public Policy, Center for Energy Studies, Rice University, 30 September 2016, http://www.bakerinstitute.org/research/chinas-evolving-oil-demand/.