China seems to be bubble surfing—two years ago it was an overheated housing market—and now the country is riding a surge of stock market enthusiasm. The stock market craze involves a much broader population base than the housing speculation did. The reason is simple: a lower barrier to entry. Houses are expensive in Chinese cities—especially in major markets like Beijing, Shanghai, and Guangzhou. In contrast, scrape up a few thousand RMB and open an online brokerage account, and you’re off to the stock trading races. No need for research, just talk to your relatives, your barber, your greengrocer, or even your taxi driver regarding what’s hot. Better yet: juice your returns (and build in a precipitous downside), trade on margin with borrowed funds. At least, that’s what far too many Chinese are doing these days…

Frenetic market activity has created enormous paper value: on the order of US$6.5 trillion over the past 12 months, according to Bloomberg. Based on World Bank and IMF data, China’s stock market capitalization currently stands just below 90% of GDP. This is significantly below pre-crisis Japan in 1989, where stock market capitalization peaked at 145% of GDP, but it still concerns us given that the rally is not underpinned by robust real economy activity.

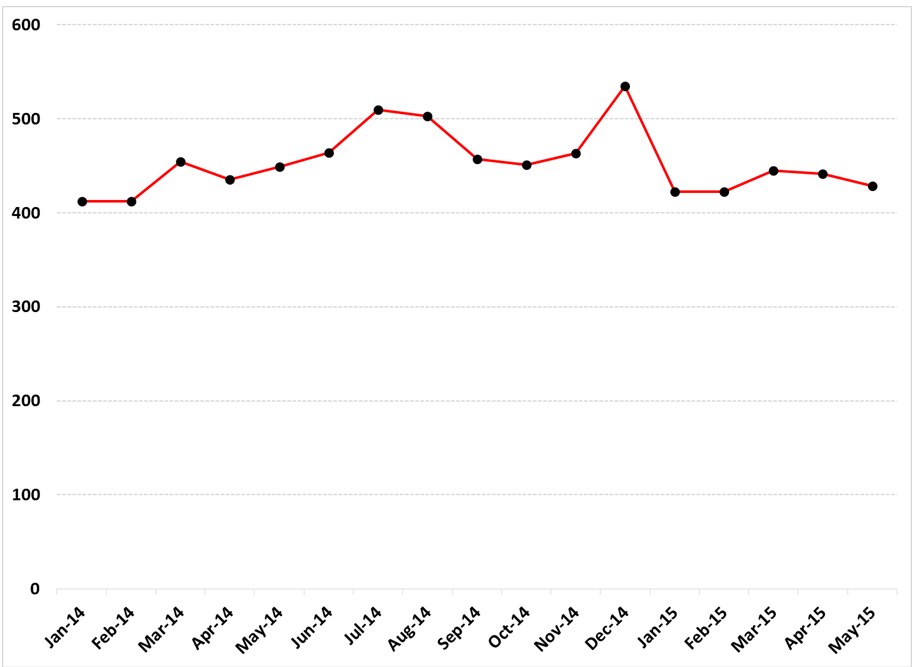

Quite to the contrary: real economy indicators suggest that the stock market is markedly decoupled from underlying economic reality. Juxtapose the massive speculative updraft in the Chinese stock market with weak electricity demand. Given China’s industrially-driven economic model, this reflects serious weakness (Exhibit 1). The Shanghai Stock Exchange has risen approximately 150% over the past year, while electricity consumption has flat-lined for the past five months and counting (Exhibit 2).

Exhibit 1: Shanghai Stock Exchange (June 2014 to June 2015)

Source: Google Finance

In contrast…

Exhibit 2: Weak Electricity Consumption

Billion kWh, monthly

Source: NBS China

Because many Chinese economic statistics remain “the mystery meat of emerging-market countries,” electricity consumption is among the best measures of real Chinese economic activity. It is one of three indicators (aside from rail cargo volume and amount of loans disbursed) that Premier Li Keqiang reportedly views as far more reliable than other official statistics because they are much more difficult to falsify. For some time now, this “Keqiang Index” has suggested substantially lower GDP growth for China than official “man-made” figures, which have themselves been ebbing.

The cautionary analysis above does not seek in any way to denigrate China’s growing day trader ranks. Save for real estate and stock speculation, non-elites have few vibrant investment opportunities. Rather, it underpins our concern that this stock market boom is unsustainable. China’s stock trading masses have created a pocket of economic and political risk that could potentially have momentous global consequences when the moment of deleveraging comes. Such events are confidence-driven and it is extremely difficult to predict when and how they will happen. But whether it unfolds next week or 12-15 months from now, even paramount leader Xi Jinping will be unable to stop it. Depending on how the de-leveraging happens and how the Chinese government and a diverse range of market participants respond, the consequences for a range of global asset classes—and perhaps political stability in China itself—will be enormous.

President Xi is the ultimate margin trader in this market. To be sure, the farmers and shopkeepers are staking risky bets, and could lose a lot if the market falls and margin calls come. But Xi and his coterie are wagering much more: his margin account is not just economic. Rather, he is effectively pledging his own political future; and in the more extreme scenarios, the Communist Party’s political legitimacy and social stability itself.

Stock market downdrafts on the heels of euphoric upswings can be devastating to far more than pocketbooks. They sow fear and destroy confidence. Confidence, in turn, is the lifeblood of economic growth and stability, as well as political stability. Indeed, financial history books are replete with examples of how sudden losses in confidence can systemically endanger an entire national economic and political system. Consider Black Tuesday and the beginnings of the U.S. Great Depression. Or more recently, consider how close the global financial system came to the precipice in August and September of 2008. The bottom line is that China now lives in “interesting” economic times. It will be an unprecedented ride in the months ahead, so buckle up and good luck! In the meantime, be careful what “mystery meat” you load up on, and don’t borrow your friend’s life savings to invest in local government debt…